Verifone Zone

VeriFone manufactures point of service (POS) terminals for credit cards and provides services and software related to processing payments. VeriFone is the market leader in POS solutions in the United States, with 60% of the retail terminal systems market.

VeriFone manufactures point of service (POS) terminals for credit cards and provides services and software related to processing payments. VeriFone is the market leader in POS solutions in the United States, with 60% of the retail terminal systems market.

What's Eating VeriFone's Profitability?

In the past, generating profit (NOPAT) growth was not a problem for VeriFone. However, new technologies in the marketplace put VeriFone's outsized profitability to an end in 2016. VeriFone's NOPAT declined 96% in 2016 over the prior year, and the company's return on invested capital (ROIC) is now 0%, which ranks in the bottom quintile of all the companies we cover. VeriFone's ROIC has been declining since 2011 to levels far below the 37% seen in 2006.

VeriFone's after-tax margins, which declined to below 1% in 2016, reflect the commoditization of the payment business. POS technology is a relatively low-development field these days, making it difficult for one manufacturer to gain a distinct edge. Sellers using pay terminals don't care who services their transactions, as long as it is done at the cheapest rate possible. This leaves little room for margin expansion going forward as VeriFone and its competitors will have to fight it out over lower fees per transaction.

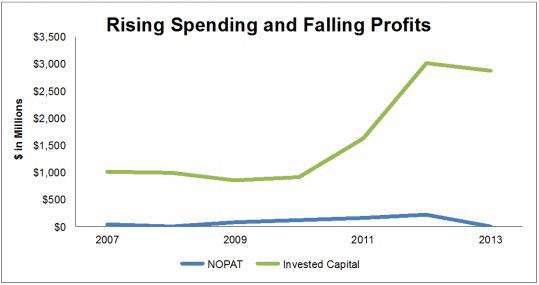

In an attempt to win over customers, VeriFone has been spending heavily in the last few years, which can be seen by the 36% annualized growth in invested capital since 2009. SG&A and R&D spending have each more than doubled over the last three years. Figure 1 highlights how this spending has not translated into profits.

Figure 1: When Increasing Capital Does Not Lead to Profits

Sources: New Constructs, LLC and company filings

VeriFone's Filings Reveal Hidden Dangers

On top of its debt, VeriFone has $479 million in total asset write-downs. Asset write-downs represent shareholder value destruction at its purest, as VeriFone is purchasing assets, causing them to decline in value, and then writing off the difference.

These write-downs represent 12% of VeriFone's market cap and 20% of its net assets. Unfortunately, write-downs are only going to increase as the new CEO is looking to slim down the company's product lineup.

Stronger Competition is Eroding VeriFone's Market Position

VeriFone competes with other POS hardware providers. One of the company's main competitors is NCR Corporation (NYSE:NCR), which also manufactures POS hardware and provides payment services. Unlike VeriFone, NCR is relatively profitable with a 7% ROIC and 7% NOPAT margins in 2016. NCR's 2014 results are also reflecting the commoditization of the POS business with increased costs and lower margins.

Related posts:

If you already have a PC and are looking to convert it to a full POS System, a bundled POS Kit is a fantastic option. Having a POS System at your business can…

If you already have a PC and are looking to convert it to a full POS System, a bundled POS Kit is a fantastic option. Having a POS System at your business can… Most of this is the Aloha default setup.NETWORK SETUP workgroup = ibertech servername = alohaboh Static IP Scheme ex 192.168.1.100 NetBIOS must be enabled over…

Most of this is the Aloha default setup.NETWORK SETUP workgroup = ibertech servername = alohaboh Static IP Scheme ex 192.168.1.100 NetBIOS must be enabled over… *Receive the stated discounted price for this year’s version of the product selected, available for a limited time if purchased through Intuit. Free shipping…

*Receive the stated discounted price for this year’s version of the product selected, available for a limited time if purchased through Intuit. Free shipping… Join millions of philatelists (or stamp collectors) in collecting, displaying and enjoying Canadian stamps. We take pride in producing beautiful and…

Join millions of philatelists (or stamp collectors) in collecting, displaying and enjoying Canadian stamps. We take pride in producing beautiful and… Allentown, PA-based point-of-sale (POS) vendor Harbortouch has disclosed a data breach affecting “a small number” of merchants using its systems. Brian Krebs,…

Allentown, PA-based point-of-sale (POS) vendor Harbortouch has disclosed a data breach affecting “a small number” of merchants using its systems. Brian Krebs,… Trust is the reason new businesses open accounts with us. Trust is the reason clients stay with us. And trust is the reason they refer their colleagues to us.…

Trust is the reason new businesses open accounts with us. Trust is the reason clients stay with us. And trust is the reason they refer their colleagues to us.…